We’re back with another update on recently-introduced tax legislation. As discussed last week, we continue to see bills reintroduced that expired at the end of the last session. Two of the more interesting proposals include repealing New York’s estate tax and another so-called “millionaire’s tax.” We’ve also been following the proposed tax changes in the Governor’s Budget proposal that came out earlier this week (see here, here, and here), and next week we’ll dedicate our update to an overall summary of the Budget proposals.

- S.B. 1434 – Circuit Breaker Tax - Property Tax Relief

This bill, a reintroduction of S.B. 3982A from last session, would create the middle-class circuit breaker tax credit. The bill would provide a personal income tax credit for certain taxpayers. If passed, the credit would be phased in over a four-year period.

- S.B. 1476 – Employer’s Deduction for Stock Options

This bill, a reintroduction of S.B. 2725 from last session, would amend Tax Law § 208 with respect to the deduction for stock options for Corporate Tax purposes. Under the proposal, the employer’s deduction amount would be based on the stock price as of the date the option is issued to the employee, rather than the price on the date of sale. The amendment would apply to taxable years beginning on and after January 1, 2022.

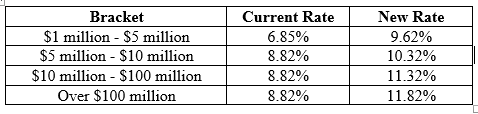

- S.B. 1513 – Millionaire’s Tax and Economic Equality Act

This bill, a reintroduction of S.B. 7677 from last session, would create the Millionaire’s Tax and Economic Equity Act of 2021. This bill would raise the personal income tax rate for individuals with New York taxable income over $1 million. Presently, the tax rate for the highest bracket tops out at 8.82%; however, this bill seeks to create new brackets with the highest bracket (income over $100 million) subject to a tax rate of 11.82%. According to the bill, the applicable tax rates would be increased as follows:

In an earlier post, we highlighted S.B. 917, which is a similar bill that would also raise the personal income tax rate for higher income individuals. However, S.B. 1513 is proposing higher rates which would begin at lower brackets. Next week we’ll be explaining the Budget proposal to apply temporary surcharges to millionaires in lieu of tax increases.

- S.B. 1516 – Repeal of Estate Tax

This bill, a reintroduction of S.B. 1157 from the last session, would repeal New York’s estate tax. The stated purpose of the bill is to encourage New York residents to continuing living and doing business in the state. This proposal seems particularly timely given recent events and the reported mass exodus New York in favor of better weather and friendlier tax jurisdictions. The bill would be effective immediately.

- S.B. 1545 – Decoupling from TCJA

This bill, a reintroduction of S.B. 7029 from the last session, would decouple from certain provisions of the federal Tax Cuts and Jobs Act (“TCJA”). If passed, New York would decouple from the 30% federal cap on business interest deduction under IRC § 163(j) for business taxpayers. Basically, the purpose of the bill would be to preserve the New York tax treatment of business interest that was in effect prior to the TCJA.

The TCJA capped the deduction of business interest expenses at 30% of business income in exchange for a five year period where businesses could immediately expense 100% of capital investments under IRC § 163(k) (“bonus depreciation”). The business interest deduction and bonus depreciation work in tandem. Since New York already decoupled from bonus depreciation, decoupling from the interest deduction cap would be a logical next step. But New York seems to be going in a different and less-logical direction. In last year’s budget, New York “doubled-down” by decoupling from the Coronavirus Aid, Relief, and Economic Security (“CARES”) Act’s temporary easing of the TCJA’s restrictions on business interest deductions.

- S.B. 1813 – Executive Compensation Penalty

This bill, a reintroduction of S.B. 1659 from the last session, would subject certain companies to an additional annual tax if its CEO receives compensation at a certain percentage greater than the median pay of all their employees (the “pay differential”). The bill would impose a 10% surtax on the company’s base tax liability if the company reports a pay differential of 100x to 250x. The tax rate would increase to a 25% surtax on the company’s base tax liability if the company reports a pay differential of 250x or greater. The tax would be imposed on companies that are subject to the United State Securities and Exchange Commission pay ratio reporting requirements.

- S.B. 1910 – Additional Sales Tax on Luxury Goods

This bill, a reintroduction of S.B. 7634A from the last session, would impose an additional 2% “sin” sales tax on certain sales of luxury goods. For example, the additional tax would be imposed on sales of certain motor vehicles over $70,000 (excluding commercial and electric vehicles), jewelry over $5,000, and clothing, shoes, handbags, and certain personal items over $1,000.